Economist John Maynard Keynes once warned that "in the long run we are all dead." He wasn't arguing against reform. He was cautioning that governments cannot expect citizens to suffer indefinitely today while dangling promises of future abundance.

That caution rings louder in Nigeria than ever before. Over three years, the government has rolled out one of its boldest economic overhauls in decades.

Fuel subsidies were scrapped. The naira was allowed to float freely.

Power tariffs jumped. Central bank rates hit multi-year peaks.

Four fresh tax laws were enacted.

Most economists accept these moves were necessary. But the real test has shifted.

The question today isn't whether the reforms made sense. It's whether ordinary Nigerians will ever taste the rewards.

That's where the newly sworn-in 15-member Ministerial Advisory Committee steps in. It could become reform Nigeria's most consequential institution.

The committee won't design fresh reforms. Those calls have mostly been made.

Its real job is far tougher: forcing the reforms already underway to deliver tangible gains in jobs, wages and living standards before people lose faith in the entire agenda.

Fixing macroeconomic chaos was always the simpler task. Converting stability into jobs and prosperity?

That's where reform attempts typically stumble or triumph.

Three years in, Nigeria's macro picture looks rosier. Foreign reserves topped $50 billion.

Capital inflows hit a record $10.37 billion in the first quarter of 2026. The exchange rate steadied after initial turmoil.

Growth picked up momentum.

Yet most Nigerians experience their economy through a different lens. They see it in rice prices, transport costs, power bills and school fees—not reserve levels or capital flows.

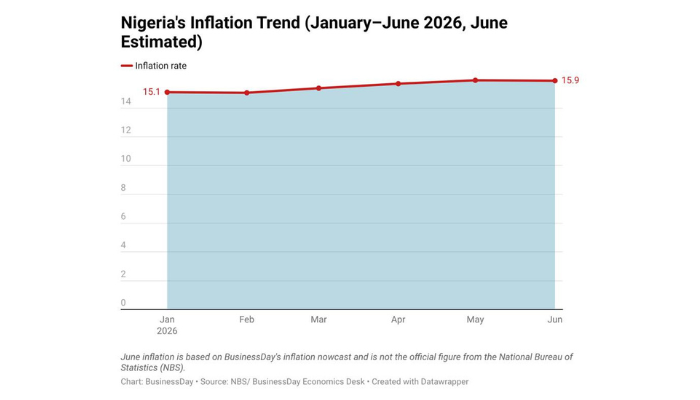

Inflation has cooled considerably from its worst point, yet prices sit well above pre-reform levels. The World Bank says the price surge plunged millions more Nigerians into poverty.

Statistics bureau data consistently shows food squeezing household budgets hardest.

This gap between stronger numbers on paper and tighter wallets at home explains why this committee matters so much. Its track record will decide if Nigeria's reforms become something people can actually feel improving their lives.

The committee won't hear arguments for bringing back fuel subsidies or fixing the exchange rate again. Those debates have largely closed.

Instead, it must make current reforms perform better.

Five critical tests will show if the committee delivers. First comes translating stability into jobs.

Investor mood has lifted. Capital streams have swelled.

Economic conditions beat where they stood three years ago. Yet employment hasn't followed suit because most new money flowed into portfolio plays rather than productive sectors capable of creating mass employment.

Unless the reforms start pulling investment toward manufacturing, farming and productive industries, stronger growth will keep bypassing the job market where it matters most. The second test involves making reforms lift ordinary household living standards, not just balance sheets.