A Nigerian entrepreneur spent months seeking bank financing for her business, facing repeated rejections before finally securing support. She credited her persistence and strong business presentation for eventually winning backing from a willing lender.

Her struggle reflects a broader challenge gripping Nigeria's small and medium-sized enterprises, which find themselves locked out of credit even as banks enjoy their strongest liquidity position in years. The banking sector's fortunes improved dramatically following a regulatory recapitalisation drive that saw lenders raise N4.7 trillion in fresh capital last March.

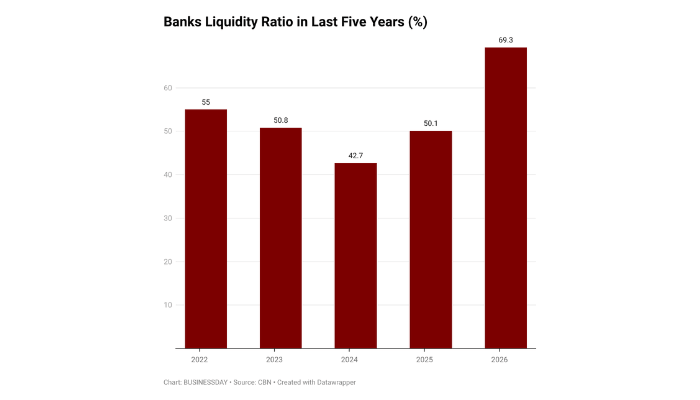

Data from the Central Bank of Nigeria (CBN) reveals the sector's liquidity ratio hit 69.27 percent in February 2026, more than double the 30 percent regulatory requirement. This marks the highest level ever recorded, surpassing the previous peak of 68 percent set in 2012.

The ratio has climbed sharply in recent years, jumping from 50.09 percent in February 2025 and 42.66 percent in February 2024. The trend underscores rapid accumulation of liquid assets across the industry.

While strong liquidity signals banking sector resilience, economists argue it masks a troubling reality. Banks prefer investing in Treasury bills, Open Market Operation (OMO) bills and government bonds rather than lending to businesses where risks run higher.

Muda Yusuf, chief executive officer of the Centre for the Promotion of Private Enterprise (CPPE), cautioned against misinterpreting the liquidity figures. "When we talk about the liquidity ratio, we are not referring only to cash," he said.

According to him, Treasury bills and other instruments comprise the bulk of liquid assets held by banks. "Cash is just a small fraction of the liquid assets that banks hold," Yusuf explained.

Banks have shifted aggressively toward government securities, he noted, drawn by attractive yields on Treasury bills and bonds. "Over time, they have also increased their investments in government bonds for the same reason," the CPPE chief told reporters.

This preference for government paper over business lending reflects institutional risk calculations, Yusuf added. "Rather than extend credit to businesses, where the risks are much higher, many banks appear to prefer investing in Treasury bills, OMO bills and Federal Government bonds," he said.

These instruments offer relatively high returns with substantially lower risk compared to corporate lending. "These instruments offer relatively high returns with much lower risk," Yusuf noted.

The executive believes this preference for government securities explains the elevated liquidity ratios observed across the sector. "The liquidity is not necessarily in cash but in other liquid assets held by the banks," he added.

The liquidity ratio itself measures banks' capacity to meet short-term obligations using liquid assets including cash, Treasury bills and government securities. The metric indicates financial stability but doesn't capture how available credit flows to the real economy.

For entrepreneurs like the woman who eventually secured financing, accessing capital remains an exhausting battle. Most small businesses continue struggling despite banks holding record buffers, highlighting a disconnect between banking sector strength and credit availability for enterprises driving economic growth.